Berkshire uses assumptions derived from its collateral database for internal modeling purposes and for completing predictive modeling assignments. Some clients prefer to conduct custom searches and analysis independently using our powerful online tools and datasets. We offer that flexibility, and we offer data hosting and analysis as a subscription service to those clients. For expert insights, customized solutions, and deeper analytics, Berkshire also provides full-service consulting through our Predictive Modeling offering.

Data Platform Overview

- Massive, up-to-date MBS and ABS databases (Agency data going back 30+ years, non-agency going back 15+ years)

- Loans mapped to pools, groups and CUSIPs (except for CAS and STACR loans originated before agencies started provided loan level detail by security)

- Secure web hosting on our public cloud platform (powerful, easy-to-use tools for defining queries, slicing and dicing)

- Rich data field content, continuously gathered, updated, normalized, verified, and validated

- Pre-defined and custom reporting and exports to Excel

- Custom model building

Coverage of Loans in Over 7,000 Non-Agency Securitizations

- Prime

- Subprime

- Alt-A

- Jumbo

- HELOC

- Manufactured Housing – Chattel and Real Estate

Complete Coverage of Agency Products

- FNMA, FHLMC, GNMA

- Megas, Giants, and Platinums

- CMOs and Re-REMICs

- CRT – STACR, CAS, ACIS, CIRT

- IO/PO Strips

- Reverse mortgages

- Pool level, Loan level performance data, Loan level credit data

Features

- Monthly Agency updates available within 60 seconds of release

- View results within browser or download

- Save and reuse custom query templates

- Excel plug-in available

- See population of pools or loans underlying a collateral filter

- Access securities by pool, CUSIP, class name, strip ID, or CMO collateral group

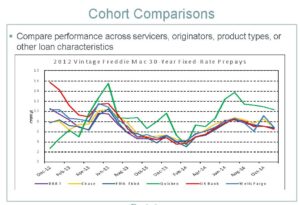

Real-Time Ad-Hoc Analysis

- Create custom queries, filters, and reports

- Analysis of cohorts or securities

- Time series analysis

- Aging curves

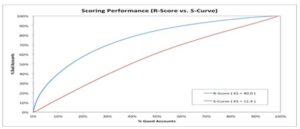

- Refinancing S-curves

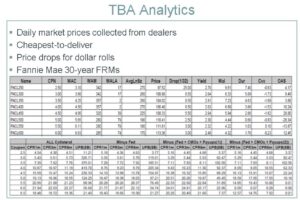

- TBA dollar roll analysis; break-even drops and financing rates

Intuitive, Yet Powerful GUI Querying Screens

- Enhanced web interface

- Easy to use query builder

- Search engine for historical queries

- User defined functions and variables

- Filter and segment by any available variable

- Programmatic access available via Python for custom workflows

Derived Variables

- Mark-to-market current LTV using FHFA indices at CBSA level

- Prepayment, default, delinquency, and buyout scores

- Refinance burnout measures

- Cheapest-to-deliver TBAs

- Float and tradable pass-throughs

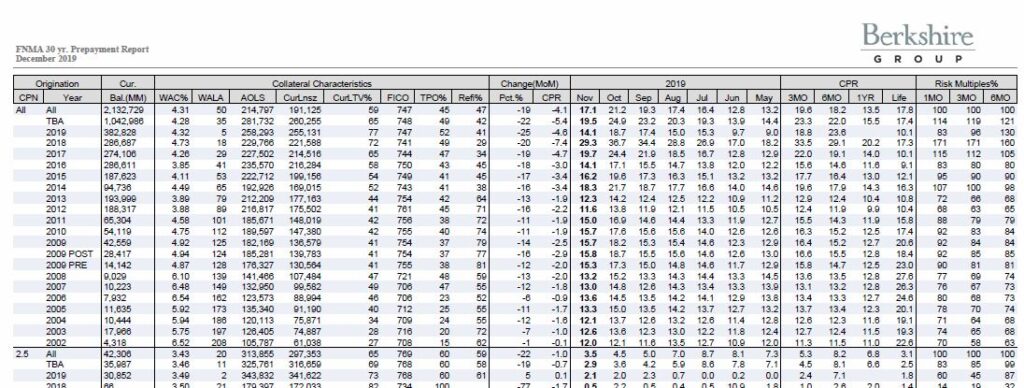

Full Suite of Prepayment Reports

- Real-time flash prepayment analytics

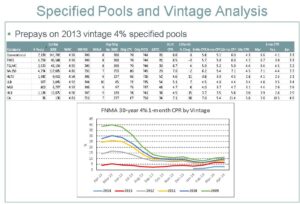

- Generics by vintage

- Servicer, issuer, and geographic indices

- Issuance volumes

- Specified pools

- Strip and mega pool performance

- Segmentation by occupancy, property type, or loan purpose

Economic Time Series Data

- Freddie Mac PMMS

- Hybrid ARM rates

- MBA application data

- MBA delinquency survey

- FHFA and Case-Shiller HPI

- Interest rates: CMT, LIBOR, swaps, prime

- Unemployment rates

Expert Insights

- Expertise from our team of industry veterans

- Advisory services to assist with interpretation and reporting

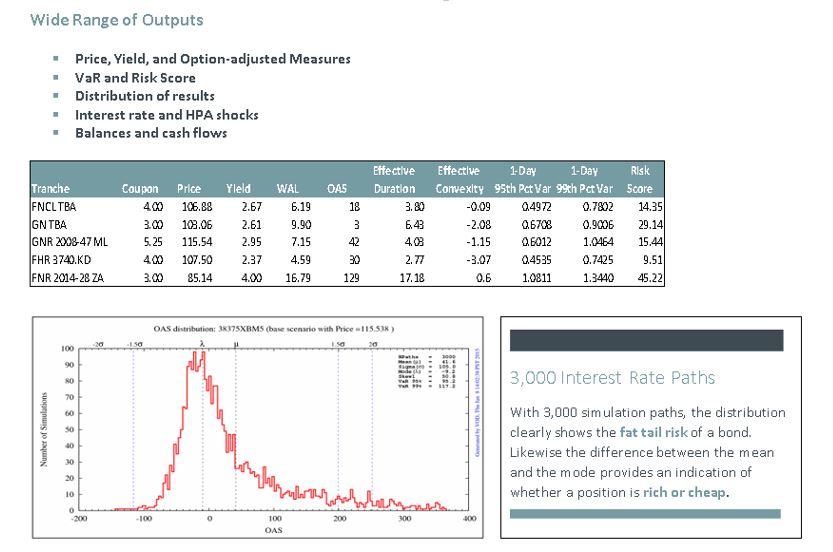

Example Outputs